Key Takeaways

- Role of Merchant Acquirer: A merchant acquirer is a financial institution that enables businesses to accept card payments by managing merchant accounts, processing transactions, and transferring funds from cardholders’ banks to the merchant, minus fees.

- Key Functions: Acquirers ensure secure transactions, provide compliance with PCI standards, manage chargebacks, and offer fraud protection, making them essential for seamless payment operations.

- Processing-agnostic POS: KORONA POS, a processing-agnostic point-of-sale system, supports small and medium-sized businesses (SMBs) in various industries, including liquor stores, vape shops, and more, by integrating with affordable payment processors.

A merchant acquirer, or an acquiring bank (or simply an acquirer), is a banking institution that processes credit or debit cards on behalf of a merchant or business.

Acquirers enable merchants and businesses of all kinds to process and receive credit and debit card payments from financial institutions that belong to a card group or network, such as Visa, Mastercard, or American Express.

Picking up the basics of payments? In this guide, we will walk you through:

What Is a Merchant Acquirer?

A Merchant Acquirer is a financial institution or bank that helps businesses accept customer payments using credit or debit cards. When a customer uses a card to make a purchase, the acquirer processes the transaction on behalf of the business, working with other parties like the card network (e.g., Visa, Mastercard) and the customer’s bank (called the issuer).

The acquirer ensures the merchant receives funds from the transaction, depositing them into the merchant’s account after deducting applicable fees. They also provide merchants with payment terminals, fraud detection tools, and compliance support for secure transactions.

Popular merchant acquirer examples include JPMorgan Chase, the largest acquirer globally, Bank of America Merchant Services, etc. These providers offer the technology and support that allow businesses of all sizes to accept online and in-store card payments.

Why a Merchant Acquirer Is Important for Businesses?

A Merchant Acquirer is crucial for businesses because it enables them to accept electronic payments, which are essential in today’s cashless and digital economy. Here’s why merchant acquirers are essential for companies:

- Enables Card Payments: Merchant acquirers allow businesses to accept debit and credit card payments, both in-store and online, which significantly increases sales opportunities. Many customers prefer paying with cards or digital wallets, and businesses without this capability risk losing them.

- Handles Payment Processing: The acquirer manages the entire transaction process—from authorization to settlement—ensuring that payments are securely and efficiently transferred from the customer to the business.

- Improves Cash Flow: By quickly settling card transactions, merchant acquirers help maintain a healthy cash flow, allowing businesses to access their funds faster than with other payment methods like checks.

- Reduces Fraud Risk: Acquirers use advanced security tools and compliance measures, such as PCI DSS, to protect businesses from fraud and chargebacks, providing peace of mind.

- Offers Reporting Tools: Most acquirers provide dashboards or portals with sales data, transaction history, and analytics, helping business owners make informed financial decisions.

- Supports Business Growth: As businesses expand, merchant acquirers offer scalable payment solutions that support multiple sales channels, currencies, and international transactions.

What Does a Merchant Acquirer Do?

Merchant acquirers assist merchants in all aspects of card and transaction processing. In the payment cycle, the acquirers’ role is to ensure that customers make their payments safely and that merchants receive the funds in their accounts. Some of the tasks of an acquiring bank include the following:

- Identifying the cardholder and verifying if the card is valid

- Ensuring the protection of the cardholder’s data

- Processing the transfer and receiving the payment from the issuing bank.

- Facilitate the payment of all payment fees charged by the card-issuing banks on behalf of the merchant

- Handle refunds, chargebacks, and returns

- Provide payment terminals to merchants

- Support payment gateways for merchants

Make payment processing smooth and easy

The primary function of an acquirer is to support the merchant by facilitating the processing of financial transactions. The merchant acquirer handles the digital dimension of the payment and all hardware needed to complete a transaction.

Most acquirers provide the merchant with a card terminal to make transactions more secure and simple. These acquirers purchase or lease POS terminals to facilitate payments for merchants.

The terminals, in turn, benefit from verification and protection by the PCI DSS (Payment Card Industry Data Security Standard). The objective of PCS DSS is to secure the entire payment card ecosystem. It ensures a secure transaction and strong protection for the merchant and the customer.

Additionally, the acquiring bank can set up an online payment gateway and enable customers to carry out their transactions safely for merchants who own an online business.

Protect merchant and customer from fraud and other illegal activities

Due to the rise of credit card fraud, cybercrime, and money laundering, securing financial credentials has become a paramount concern for acquirers. Processing financial information is not risk-free. Merchant acquirers have therefore beefed up their security by implementing measures to prevent fraud and chargebacks against the merchant.

Generally, merchants are held responsible for chargebacks on credit or debit cards. This occurs when the payment intended to be sent to the merchant’s bank account is transferred to the customer’s bank account.

If you run a retail store, chances are, you’ve witnessed a customer’s contactless payment that was rejected, and the customer was forced to use the chip and pin. In this case, the cardholder’s issuing bank or your acquiring bank may have declined the transaction due to security concerns and avoided chargebacks.

In addition, acquirers also take strong measures to prevent illicit activity such as money laundering. They, therefore, perform checks on merchants to ensure the reliability of their business and the funds they receive. These measures are intended not only to protect customers but also other businesses, especially the reputation of merchant acquirers.

Merchant Acquirer vs. Payment Processor

For retail business owners, understanding the difference between a Merchant Acquirer and a Payment Processor is key to setting up smooth card payment systems. While both help businesses accept card payments, their roles differ. Here’s a clear, simple explanation:

Merchant Acquirer: A financial institution (often a bank) that provides a merchant account and facilitates card transactions. It’s the “banking” side of the process.

What it does:

- Opens and manages your merchant account where funds from card payments are deposited.

- Communicates with the cardholder’s bank and card networks (e.g., Visa, Mastercard) to approve transactions.

- Transfers funds to your business account, minus fees.

- Ensures compliance with payment regulations (like PCI standards).

- Handles chargebacks or disputes.

- JPMorgan Chase or Bank of America Merchant Services.

Payment Processor: A company that handles the technical side of processing card transactions, acting as a middleman.

What it does:

- Provides the technology (e.g., payment terminals, online gateways) to accept card payments.

- Transmits transaction data between your business, the acquirer, and card networks.

- Offers fraud detection tools and customer support for payment issues.

- May bundle services with an acquirer for simplicity.

- Stripe, Square, or PayPal are processors.

Why it matters: Processors make it easy to accept in-store or online payments with user-friendly tools.

Key Difference: The acquirer is the financial partner who manages your funds and ensures they reach your account. The processor is the tech partner who handles the transaction process. Many businesses work with both, as some processors (like Stripe) partner with acquirers to offer a complete solution.

How Does Payment Processing Work? A Step-by-Step Guide

Knowing the different steps of transferring money from your customer to your company is helpful as a merchant. If a discrepancy occurs during a transaction, it helps you determine the problem and how to address it.

There are two steps to processing payments: The first is approving the sale or authorization. The second is clearing the transaction or depositing the funds into the merchant’s account.

The approval process goes roughly like this:

- Your customer buys an item in your store and pays by credit or debit card. They insert or tap their card into the POS payment terminal.

- The transaction information passes through the payment gateway, which encrypts the card data to keep it private.

- This information is then transmitted to the merchant acquirer.

- The acquiring bank sends a notification to the card network (i.e., Visa or MasterCard)

- Next, the card network transfers the transaction information to the customer’s issuing bank to ensure that the latter has enough money on their card to pay for their items.

- The issuing bank approves or rejects the transaction and submits a response to the card network.

- The card network relays that information to the merchant acquirer, which transmits it to the payment gateway, informing the merchant whether the transaction is approved or disapproved.

- The issuing bank places a hold on the cardholder’s account, which will turn into a direct debit after the transaction is finalized.

The deposit of the funds to the merchant’s account

- The point-of-sale system or card terminal prints a receipt to validate the customer’s purchase.

- The funds are transferred to the merchant’s account 24-72 hours later.

Some of the terms related to payment processing can be confusing and difficult to understand. Let’s break them down:

Payment gateway

The payment gateway is a must-have technological feature in retail or wholesale. It is the online version of a point of sale system that connects your website to the payment processor. The payment gateway is also used to accept credit or debit cards. This system takes care of the technical side of the transaction and facilitates the payment for your customers.

Payment processor

The payment processor is the company that handles the transaction between the customer and your business. This institution transmits the credit or debit card information to your bank and the customer’s card-issuing bank.

The payment processor handles card limits, card validity, insufficient funds on a card, or stolen cards. However, it is important not to confuse a merchant acquirer with a payment processor.

While some financial institutions act as both acquirers and processors, there has been a shift in recent years toward using separate third-party processors. Unlike acquirers, which handle transactions and communications between banks and hold funds at various locations, payment processors are solely responsible for processing payments.

Processors simply manage the technical services with merchants but do not take financial responsibility for those services. Only the merchant acquirer can do that. In short, the processor can be considered the acquirer’s technical arm.

Payment processors

giving you trouble?

We won’t. KORONA POS is not a payment processor. That means we’ll always find the best payment provider for your business’s needs.

Merchant account

A merchant account is a bank account intended to accept online payments and payments made by bank cards. It requires an acquiring bank.

Difference Between an Acquiring Bank and an Issuing Bank

The acquiring bank processes the customer’s card or online transaction information, while the issuing bank provides consumers with the credit or debit card used in stores.

The acquiring bank does not communicate directly with the consumer’s card-issuing bank during payment processing.

The issuing bank is associated with a card network, which acts as an intermediary between the acquirer and the issuing bank.

Examples of Merchant Acquirers

Examples of prominent merchant acquirers include:

- FIS (Worldpay)

- JPMorgan Chase

- Fiserv (First Data)

- Bank of America Merchant Services

- Global Payments

- Adyen

- Elavon

- Barclaycard Business

- Lloyds Bank Cardnet

These entities play a crucial role in the payment ecosystem by managing merchant accounts, handling transaction authorization requests, and settling funds, often working with payment processors. Some smaller operations can use payment facilitators like PayPal or Venmo to accept electronic payments.

How to Choose an Acquirer for Your Business?

Below is a detailed guide to help small retailers select the best acquirer for their needs.

1. Assess Your Business Needs

- Understand Your Transaction Volume: Estimate your monthly card transaction volume (e.g., $5,000 or $50,000). High-volume retailers may benefit from acquirers offering lower per-transaction fees, while low-volume businesses might prioritize flat-rate pricing.

- Determine Payment Types: Identify the payment methods you’ll accept (credit/debit cards, mobile payments like Apple Pay, or online payments). Ensure the acquirer supports all relevant card networks (Visa, Mastercard, Amex, etc.).

- Evaluate Sales Channels: If you operate in-store, online, or both, choose an acquirer with solutions for your channels. For example, online retailers need robust payment gateway support, while brick-and-mortar stores require reliable POS terminals.

2. Compare Fees and Pricing Structures

Understand Fee Types: Acquirers charge transaction fees (e.g., 2.5% per sale), monthly account fees, setup fees, or chargeback fees. Ask for a clear breakdown to avoid surprises.

Look for Transparent Pricing: Some acquirers, like JPMorgan Chase, provide detailed fee schedules. Avoid those with hidden costs, such as early termination fees.

Consider Flat vs. Interchange-Plus Pricing:

Flat-Rate: Simple, predictable fees (e.g., 2.9% + $0.30 per transaction, like Square). Ideal for small retailers with low volumes.

Interchange-Plus: A percentage plus the card network’s fee (e.g., 0.5% + interchange). Better for high-volume retailers, as it can be cheaper.

Negotiate for Better Rates: If you process significant volumes, negotiate fees with acquirers like Bank of America Merchant Services, which may offer discounts.

3. Check Compatibility with Payment Processors

- Many acquirers partner with payment processors (e.g., Stripe works with multiple acquirers). Ensure the acquirer integrates with your preferred processor or POS system (e.g., Shopify, Clover).

- Verify if the acquirer provides their own processing tools or requires a third-party processor, as this affects setup complexity and costs.

4. Prioritize Security and Compliance

- PCI Compliance: To protect customer data and avoid penalties, choose an acquirer that complies with Payment Card Industry Data Security Standards (PCI DSS). For example, First Data (Fiserv) offers robust PCI support.

- Fraud Protection: To minimize risks, look for acquirers with advanced fraud detection tools, like tokenization or real-time monitoring. Stripe’s Radar system is a strong example.

- Chargeback Support: Select an acquirer that assists with managing chargebacks (disputed transactions), as these can be costly for small retailers.

5. Evaluate Technology and Support

- Hardware and Software: Ensure the acquirer provides modern payment terminals (e.g., contactless-enabled) or online gateways that suit your business. For instance, Global Payments offers versatile POS solutions.

- Ease of Integration: Check if their systems integrate easily with your existing setup (e.g., accounting software like QuickBooks).

- Customer Support: Opt for acquirers with 24/7 support via phone, email, or chat. Small retailers often need quick resolutions for payment issues. Read reviews on platforms like Trustpilot to gauge support quality.

6. Assess Scalability and Flexibility

- Choose an acquirer that can grow with your business. For example, if you plan to expand internationally, select one like Global Payments, which operates in 30+ countries.

- Ensure they offer flexible contract terms. Avoid long-term contracts with high cancellation fees, especially if you’re testing the waters.

7. Research Reputation and Reliability

- Investigate the acquirer’s track record. Established players like JPMorgan Chase (processing over $1 trillion annually) or Bank of America (12% market share) are reliable choices.

- Check for uptime guarantees to avoid transaction downtime, which can frustrate customers.

- Look at user reviews on sites like Capterra or posts on X to confirm the acquirer’s performance with other small businesses.

8. Request Quotes and Test Services

- Contact multiple acquirers (e.g., JPMorgan Chase, Stripe, First Data) for quotes tailored to your business size and needs.

- Ask for a trial period or demo to test their systems, ensuring they meet your operational requirements.

9. Consider Bundled Services

Some acquirers, like Square or Stripe, combine acquiring and processing services, simplifying setup for small retailers. These all-in-one solutions are beginner-friendly but may have higher fees for larger businesses.

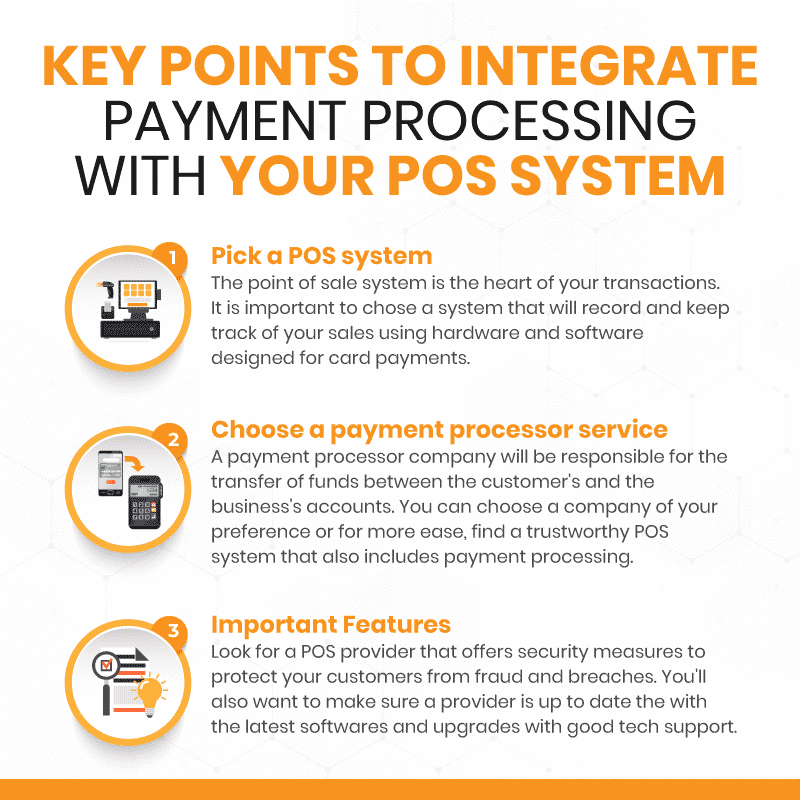

How to Integrate Payment Processing With Your POS System?

Integrating a point-of-sale system with payment processing has many advantages that need not be repeated. The process is simple and can reap tremendous dividends when done.

Pick a POS system

Without a POS system, there is no POS credit card processing. Consider your point of sale system as the mastermind of your payment processing – retrieves the entries placed in the credit card reader and interprets them as financial transactions for your business. So, among many other things, a point of sale is at the heart of your payment operation.

As the POS system records sales directly as they occur, you need hardware and software that identifies your card reader. If you don’t have a point-of-sale system yet, now is the time to consider an immediate setup. Talk to one of our product specialists for information on how to find an affordable payment processor.

Speak with a product specialist and learn how KORONA POS can power your business.

Choose a payment processor service

A payment processor is the company responsible for processing credit cards, including communicating with all parties, ensuring security, and facilitating the final transfer of funds between banks. Some of these processors provide payment terminals to merchants or card readers that are compatible with their services.

If you decide to contact a payment processing company other than the one that installed your POS system, you’ll need to do some thorough research. Check both providers’ hardware and software and ensure they are compatible. If you don’t know how to do this, contact your POS provider for help.

However, if you use the same vendor for your POS and card processor, you can leave it up to the company to manage updates and compatibility. But in this case, make sure you have chosen a trustworthy company that can assist you with software upgrades and doesn’t gouge your business with its payment processing pricing.

Look for extra features, security, and customer service

With many online transactions today, customers are more vulnerable to fraud. Therefore, choose a POS provider that offers security measures tailored to your needs, including protections against breaches.

Also, ensure your POS software provider is equipped with the latest technological advances. With KORONA’s software-as-a-service, you’ll receive any software updates and upgrades without ever having to request them or pay a single penny. Ensure that your company only has the best small business POS system. Some of the latest features that KORONA POS offers include:

- Fast transactions and user-friendly

- Integrated payments

- Customer-facing display

- Multi-store and franchise features

- Business and marketing automation

- Advanced inventory management

- Smart inventory reporting and analytics

- Payroll and accounting integration

- Commission and tip management

- Employee and cashier permissions

- Offline transactions and back-office access

- Promotions and point-based loyalty programs

Choose The Right Payment Processor For Your Retail Business With KORONA POS

KORONA POS is a point of sale system designed to serve a range of retailers, including liquor stores, vape shops, CBD retailers, and convenience stores. While not a payment processor, KORONA POS helps businesses connect with the right processor based on industry needs. It offers flexibility and compatibility with various merchant service providers.

KORONA POS offers processor-agnostic software. Retailers can shop for the most competitive rates and services. This freedom ensures businesses aren’t locked into one provider, enabling them to choose the best payment solution while benefiting from a robust, retail-focused POS system.

Choose KORONA POS to simplify payment management and increase your retail sales. Try KORONA POS for free now by clicking on the button below.