Key Takeaways:

- Ease of Setup and Accessibility: Third-party payment processors allow businesses, especially small ones, to start accepting credit and debit card payments quickly without needing their own merchant account.

- Cost Efficiency with Trade-offs: They typically offer lower upfront fees and no monthly charges, but transaction fees can be higher (around 2-3% plus a flat fee per transaction), and funds may take days or weeks to transfer.

- Flexibility in Payment Options: They support various payment methods, including cards, digital wallets, and international currencies.

- Potential Risks and Limitations: Accounts can be frozen or terminated if deemed high-risk (e.g., due to chargebacks), and merchants have less control over the payment process. Therefore, it is essential to review terms for hold periods and dispute resolution policies before committing.

Running a retail business today means giving customers fast, secure, and flexible ways to pay. That’s where third-party payment processors come in. Instead of setting up a costly and complex merchant account with a bank, retailers can use a payment processor to accept credit cards, debit cards, and digital wallets with minimal setup.

In this blog, we’ll break down what a third-party payment processor is, how it works, and why choosing the right one can streamline your checkout process, improve customer experience, and help your business grow.

To make the checkout process frictionless, retail stores, eCommerce merchants, vendors, and service providers turn to third-party payment processors. However, the use of payment processors is not without cost. There are fees charged on every transaction.

But with so many third-party payment processors on the market, which one is right for your business? What is the actual role of payment processors, and how do they work? Does your retail store have the right POS software to integrate your choice’s payment processor? Check out the answers to all these questions in the sections that follow.

What Is a Third-Party Payment Processor?

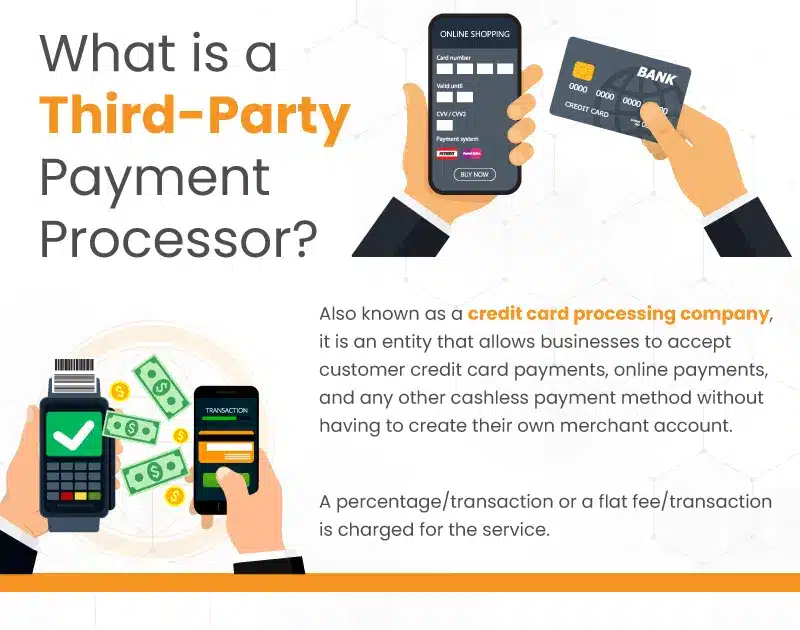

A third-party payment processor, also known as a credit card processing company, is an entity that allows businesses to accept customer credit card payments, online payments, and any other cashless payment method without having to create their own merchant account. A payment processor is also the third-party processor of ACH bank transfers.

Payment processors charge a fee for their services. This fee is usually a percentage per transaction or a flat fee per transaction.

Other pricing plans include a flat monthly fee with a lower per-transaction authorization fee. Merchants with high transaction volumes can usually negotiate better rates with payment processors.

How Does Third-Party Payment Processing Work?

Customer checkout: Customer taps/swipes/enters card or uses a digital wallet (Apple Pay, Google Pay, etc.).

Data capture and encryption: Your POS or website captures card data and immediately encrypts it or sends it to the processor’s hosted page/iframe to reduce PCI scope.

Tokenization (optional but common ): If you want to store cards on file (recurring billing, one-click checkout), card data is exchanged for a token. The token is useless to attackers.

Payment gateway → payment processor: The gateway (software) sends the encrypted details to the third-party processor, which prepares the authorization request.

Routing to card network: Processor routes the authorization request to the appropriate card network (Visa, Mastercard, etc.).

Issuer check & authorization: The customer’s issuing bank checks funds/fraud rules and returns an approval or decline, plus an authorization code.

Response returned to merchant: The approval/decline returns along the same path to your gateway/POS and the transaction is completed (receipt printed or checkout confirmed).

Capture vs Authorization: Authorization places a hold on funds. Capture (often immediate for retail) finalizes the charge. In some workflows, capture happens later (hotel, car rental).

Batching and settlement: The processor batches captured transactions and submits them to the card networks for settlement (usually at the end of the day).

Funds flow: Issuing bank → card network (minus interchange/assessments) → acquirer/processor → for third-party processors often into the processor’s account, then disbursed to the merchant’s bank account according to the PSP’s payout schedule.

Reconciliation: Processor provides settlement reports and statements you use to reconcile sales vs. payouts.

Chargebacks & disputes: If a customer disputes a charge, the issuer initiates a chargeback, which is routed back to the processor. The processor notifies you and manages the representation or dispute response processes.

| Feature / Concern | Third-party payment processor (PSP / Aggregator / PayFac) | Traditional merchant account (Acquirer + your MID) |

|---|---|---|

| Onboarding time | Very fast — minutes to days; automated onboarding. | Slower — days to weeks; manual underwriting. |

| Account ownership | Sub-merchant under processor’s master account (often no separate MID). | You get your own Merchant ID (MID) with acquiring bank. |

| Pricing model | Often flat-rate or blended fees; easy to understand but less transparent. | Usually interchange-plus or tiered; more transparent and negotiable at scale. |

| Fee transparency | Lower visibility into interchange + markup. | High transparency; easier to audit interchange + markup. |

| PCI scope | Can be reduced with hosted solutions (less burden on you). | Often larger PCI responsibilities unless gateway is used. |

| Control & customization | Limited control over routing, settlement rules, or dispute escalation. | Greater control: custom routing, multi-acquirer setups, tailored pricing. |

| Payout speed | Often next-day, or configurable; some offer instant payouts (fees may apply). | Typically 1–3 business days; can be negotiated for faster funding. |

| Reserve / holds risk | Higher chance of rolling reserves, holds, or freezes for new/high-risk sellers. | Possible, but reserves are negotiated and clearer in the contract. |

| Chargeback handling | PSPs provide dispute tools; may act as Merchant-of-Record in some cases. | You manage disputes directly with your acquirer; clearer legal relationship. |

| Best for | Small/medium retailers, omnichannel sellers, those needing fast setup & simple UX. | High volume merchants, businesses wanting better pricing control or lower per-transaction cost. |

| Integration options | Rich SDKs, hosted checkout, tight POS integrations and bundled hardware. | Gateway + acquirer integrations; more options but may need more technical work. |

| Contract & termination | Flexible; month-to-month options common. | Often contractual (term agreements) but negotiable for volume customers. |

| Reporting & reconciliation | Modern dashboards, but statements may be aggregated. | Detailed interchange-level statements — helpful for cost analysis. |

| Regulatory / geographic coverage | Many PSPs support international cards and multi-currency, but fees vary. | Acquirers can offer direct local acquiring in many countries; may be better for large cross-border volume. |

Basic Terminology for Understanding Payment Processors

To further understand the functioning of third-party payment processors, you need to know the basic terminology. Here are some terms you need to understand:

The acquiring bank

The acquiring bank, or merchant acquirer, is the financial institution that issues the merchant account for accepting credit and debit cards. The acquirer receives payments from the issuer through the payment processor and credits batch transactions to the merchant account.

Merchant account

A merchant account is a commercial bank account that allows a business to accept and process electronic payment card transactions.

It is the bank account on which the issuer’s money, on behalf of the cardholder, is deposited to pay for batches of credit card transactions of the merchant’s customers within one to three days after a sales transaction.

When a customer swipes their credit or debit card to pay for a transaction, the card processor sends the transaction details to your merchant account.

Your merchant account provider confirms that sufficient funds are available from the customer’s card issuer. Once funds are approved, your merchant account provider advances your company the funds for that transaction.

The issuer

The issuer, or issuing bank, is the bank that delivers the credit card to customers to pay for purchases. Through a payment processor, this issuing bank pays the acquirer responsible for paying the merchant for the credit card transactions.

The issuer then receives the funds from the cardholder, who pays the credit card statement. The issuer is often the same as the customer’s bank.

Payment gateway

A payment gateway differs from a processor because it is a fast and secure method for online payment data. A payment gateway includes a point of sale (POS) card reader and online portal software technology for eCommerce transactions. It authorizes and enables payments from a customer to a merchant or vendor.

PCI compliance

The Payment Card Industry Data Security Standard (PCI DSS) is a set of requirements to ensure that all companies that process, store, or transmit credit card information maintain a secure environment.

POS System

A point of sale system, or POS, is where customers pay for products or services in your store. Simply put, every time a customer makes a purchase, they make a POS transaction.

Finding the right point of sale system for your business can eliminate many manual entry and reporting errors. Many of these systems are similar, but key features stand out in the different systems that can make all the difference. Choosing a third-party payment processor also depends on the type of POS software you have.

Pros and Cons of a Third-Party Payment Processor

A third-party payment processor, such as Stripe, Square, or PayPal, is a company that provides a single, shared merchant account for thousands of businesses. Instead of a retailer having a direct relationship with an acquiring bank, the processor acts as a middleman, aggregating transactions under its umbrella. This “one-to-many” model has distinct pros and cons.

Pros: The Case for Convenience and Speed

Lower Barriers to Entry and Faster Onboarding: This is the most significant advantage. A third-party processor bypasses the lengthy and rigorous underwriting process to get a traditional merchant account. A retailer can sign up online, get approved instantly, and accept payments within minutes. This is a game-changer for new businesses, seasonal businesses, or those with limited financial history.

Simplified, Predictable Pricing: These processors almost exclusively use a flat-rate pricing model (e.g., 2.9% + $0.30 per transaction). This offers incredible clarity and predictability. A business owner doesn’t need to understand complex interchange fees, tiered rates, or the nuances of card types. The cost is the same for a Visa, Mastercard, or American Express, simplifying financial forecasting and reconciliation.

No Upfront or Recurring Fees: Most third-party processors do not charge monthly, annual, PCI compliance, or early termination fees. This “pay-as-you-go” structure is ideal for low-volume or startup businesses that want to keep overhead costs to a minimum. You only incur a cost when you make a sale.

Integrated Technology and Features: These providers are often technology-first companies. They build robust, all-in-one platforms that include payment processing, POS software, eCommerce tools, virtual terminals, invoicing, and reporting. Their APIs are often well-documented and developer-friendly, seamlessly integrating existing systems (like e-commerce platforms or accounting software). This centralization reduces the need to manage multiple vendors.

Robust Security and PCI Compliance Relief: Third-party processors are responsible for maintaining PCI DSS compliance, the industry’s data security standard. They use advanced security measures like tokenization and encryption to protect sensitive cardholder data. By handling this responsibility, they significantly reduce the retailer’s compliance burden and potential liability. The retailer still plays a role, but the processor shoulders the heaviest lift.

Cons: The Hidden Costs of Convenience and Control

Higher Overall Costs for Growing Businesses: The flat-rate pricing model, while simple, is rarely the most cost-effective for a business with significant volume. The flat fee covers the processor’s risk and profit margin for all card types, including expensive “non-qualified” rewards cards. A growing retailer processing hundreds or thousands of monthly transactions will almost certainly pay more than they would on a transparent interchange-plus model with a traditional merchant account.

Increased Risk of Account Holds and Freezes: Because a third-party processor aggregates thousands of merchants under one master account, it’s highly sensitive to risk. Their fraud detection systems are often automated and can be overly cautious. A sudden spike in sales, an unusually large transaction, or many chargebacks can trigger an immediate account hold or freeze without warning. This can be devastating for a business, as it cuts off access to revenue and can take days or weeks to resolve.

Lack of Dedicated Customer Support and Advocacy: Due to the sheer volume of their clients, third-party processors often have a “self-service” model for customer support. You might be directed to online forums or a knowledge base rather than a dedicated account manager. Getting a live person who understands your business can be incredibly difficult and frustrating when a critical issue arises—like a frozen account or a technical glitch. You also have no advocate to represent your business to the card networks in a chargeback dispute.

Delayed Payouts and Reduced Cash Flow: While the transaction is instant, the settlement of funds is often not. Third-party processors hold funds in their shared merchant account and pay out to the retailer’s bank account on a schedule, which can be daily, weekly, or bi-weekly. This delay can negatively impact a business’s cash flow, especially when compared to traditional merchant accounts that may offer next-day or even same-day funding.

Less Flexibility and Control: A retailer using a third-party processor is subject to their terms of service, which can be unilaterally changed. You have less control over the user experience (e.g., you can’t white-label the payment page) and are limited by the hardware and software they provide. This lack of control can become a bottleneck as a business matures and its needs become more complex and specialized, for instance, with custom loyalty programs or integrated inventory management.

Examples of Third-Party Payment Processors

Here are some examples of payment processors:

- Amazon Payments

- BitPay

- WePay

- Stripe

- Wise

- QuickBooks Payments

- PayPal

- 2Checkout

- Authorize.Net

- Secure Payment Systems

- Square

How to Choose the Right Processor?

Here is a deep dive into the steps involved in selecting the right payment processor for your retail business.

Step 1: Conduct a Holistic Needs Assessment

Before you start looking at providers, you must understand your business’s payment DNA. This goes beyond “I need to accept credit cards.”

Analyze Your Transaction Profile

Go granular. What is your average transaction size? What is your monthly and annual transaction volume in terms of count and total dollar value? Do you have seasonal spikes? Do you have a lot of low-value transactions or a few high-value ones? This analysis is crucial because it will dictate the most cost-effective pricing model. A business with high transaction volume and low average order value (AOV) might benefit from a flat-rate model. In contrast, an interchange-plus model might better serve a business with a high AOV and low volume.

Identify Your Payment Channels

Do you operate a brick-and-mortar store, an e-commerce site, or both (omnichannel)? Do you take payments over the phone? Do you need a mobile point-of-sale (mPOS) solution for pop-up shops or trade shows? Each channel has different hardware and software requirements and may have different processing fee structures.

Define Your Customer’s Payment Preferences

Don’t just assume your customers want to pay with Visa or Mastercard. Are they using digital wallets like Apple Pay or Google Pay? Is “Buy Now, Pay Later” (BNPL) a growing trend in your market? Are cryptocurrencies a relevant option for your customer base? A frictionless checkout experience with various payment methods can significantly boost conversion rates.

Assess Integration and Ecosystem Needs

Your payment processor is not an island. It needs to integrate seamlessly with your existing business software. What is your Point of Sale (POS) system? What about your e-commerce platform (e.g., Shopify, WooCommerce)? Do you need it to sync with your accounting software (e.g., QuickBooks, Xero) and Customer Relationship Management (CRM) system? Poor integration leads to manual data entry, reconciliation errors, and operational inefficiency.

Step 2: Decode the Pricing Models and Scrutinize the Fine Print

Many businesses get a raw deal here. Payment processing fees are complex and can be intentionally opaque. You must understand the different pricing models and where hidden fees might lurk.

Interchange-Plus Pricing

This is the most transparent and often cost-effective model for medium to high-volume businesses. The fee is broken down into two components: the interchange fee (a percentage + a per-transaction fee set by the card networks, like Visa and Mastercard) and the “plus”, the payment processor’s fixed markup. You see precisely what the wholesale cost and the processor charge you.

Tiered Pricing

Avoid this model if possible. It’s often a source of hidden costs. Transactions are categorized into “qualified,” “mid-qualified,” and “non-qualified” tiers, each with its own rate. The processor sets the rules for what falls into each tier. For example, a swiped, non-rewards debit card might be “qualified” with a low rate, but a manually entered, rewards credit card could be “non-qualified” with a much higher rate. This model makes it incredibly difficult to forecast your costs.

Flat-Rate Pricing

This is the simplest model, where you pay a single, fixed percentage per transaction, regardless of the card type or processing method. It is often a good fit for small businesses with low, unpredictable volumes and/or low average transaction values because it offers predictability. However, for a growing company, this simplicity comes at a price; you’ll likely pay more in the long run than with an interchange-plus model.

Subscription or Membership Pricing

This model involves a fixed monthly fee in exchange for lower per-transaction rates. This can be highly beneficial for high-volume merchants, as the cost savings on individual transactions can quickly outweigh the monthly fee.

Beyond the Models: Look for Hidden Fees. Don’t just focus on the per-transaction rates. Ask about:

- Gateway Fees: A separate fee for using the payment gateway (the technology that transmits the data).

- Monthly/Annual Fees: A flat fee to maintain the account.

- PCI Compliance Fees: A fee for ensuring your business meets the Payment Card Industry Data Security Standard.

- Chargeback Fees: A fee for each disputed transaction.

- Statement Fees: A fee for providing your monthly statement.

- Early Termination Fees: A penalty for ending your contract early.

Step 3: Prioritize Security and Compliance (The Non-Negotiables)

Your reputation and your customers’ trust are on the line. Security and compliance are not optional extras.

- PCI DSS Compliance: Ensure your processor is fully PCI DSS compliant and has a clear plan to help you achieve and maintain compliance. This set of security standards is designed to protect cardholder data. Non-compliance can lead to hefty fines and reputational damage.

- Fraud Prevention Tools: A good processor offers more than basic fraud screening. Look for advanced features like tokenization (replacing sensitive card data with a unique, secure token), 3D Secure for e-commerce transactions, and AI-powered fraud detection that analyzes transaction patterns in real time.

- Chargeback Management: Chargebacks are a significant threat to a retailer’s profitability. Ask what tools the processor provides to help you fight illegitimate chargebacks and how their system can help you provide the necessary evidence to the card networks.

Step 4: Evaluate for Usability, Support, and Scalability

A great rate is useless if the system is difficult to use or you can’t get help when needed.

- User Experience and Hardware: Is the system intuitive for your staff? Are the POS terminals easy to use and reliable? Does the hardware look professional and modern? For e-commerce, is the checkout process seamless for the customer?

- Customer Support: This is critically important. A frozen terminal on a busy Saturday afternoon can cost you thousands in lost sales. Ask about their support hours (24/7 is a must for retail), the average wait time, and whether you’ll speak to a knowledgeable human or a chatbot. Look for a dedicated account manager if your business volume warrants it.

- Scalability: Choose a processor that can grow with you. Does the system handle a high volume of transactions without performance degradation? Does it offer features you might need in the future, such as multi-location management, currency conversion, or international payment processing? Ask for a platform roadmap to see what new features are being developed.

Step 5: The Final Due Diligence: Reference Checks and Negotiations

You’ve narrowed it down to a few top contenders. Now it’s time to dig deeper.

- Ask for References: Don’t just rely on online reviews. Ask the processor for a few references from businesses of a similar size and industry to yours. Ask the references specific questions about their experience with customer support, hidden fees, and system reliability.

- Negotiate Your Terms: Remember, everything is negotiable. Use your transaction profile data to your advantage. If you have a high volume, leverage that for a better rate. Don’t be afraid to ask for a reduction in monthly fees, a lower chargeback fee, or a waiver of the PCI compliance fee. Push for a month-to-month or short-term contract to start, so you can easily exit if things don’t work out as promised.

How POS and Payment Processors Work Together?

A white label POS system and a payment processor work together to complete a sale seamlessly. When a customer is ready to pay, the POS system calculates the total and prompts for payment.

Once the customer swipes, taps, or inserts their card, the POS securely passes that payment information to the payment processor.

The processor then routes the transaction through the card networks (like Visa or Mastercard) to the customer’s issuing bank for approval.

The bank checks for sufficient funds or credit, performs fraud checks, and sends back an approval or a decline. That response flows back through the processor to the POS, which instantly updates the cashier and customer.

After approval, the POS records the sale, while the processor ensures the funds are eventually deposited into the merchant’s account.

In this way, the POS manages the customer-facing transaction, while the payment processor handles the behind-the-scenes movement of money—working together to complete the sale smoothly and securely.

Integrate Your Choice of Payment Processing With KORONA POS

Running a retail business in a high-risk industry—whether it’s liquor, vape, smoke, convenience, or cannabis comes with unique challenges, especially when it comes to payment processing. That’s where KORONA POS makes a difference.

Unlike many point-of-sale providers that lock you into one payment processor, KORONA POS allows you to integrate with the processor of your choice.

Reliability and compliance are crucial for high-risk retailers. KORONA POS is built to support secure, PCI-compliant transactions while giving you the tools to stay on top of your operations.

From age verification and ID scanning to customizable reports, advanced inventory management, and multi-store scalability, the system is designed to fit the demands of regulated industries. Plus, the open payment integration ensures that if your current processor changes policies or fees, you can easily switch without overhauling your entire POS.

With KORONA POS, you’re not just getting a point-of-sale solution—you’re getting a partner that adapts to your industry’s needs. Whether scaling a cannabis dispensary, managing multiple convenience stores, or running a busy liquor shop, KORONA POS ensures smooth transactions, detailed insights, and the flexibility to keep your business moving forward.

FAQs: Third-Party Payment Processors

What are examples of payment processors?

Some popular processors include PayPal, Square, ChargeBee, Wise, Stripe, 2Checkout, WePay, etc.

Is PayPal a third-party payment processor?

Yes, PayPal is a third-party payment processor. However, in 2013, it acquired Braintree, a separate eCommerce payment processing service and gateway integrating with PayPal.

Is Apple Pay a third-party payment processor?

Apple Pay is not a payment processing service system. It is a mediator or digital wallet that stores private data and allows the user to pay through a third-party processing system.